Fed Rate Hikes (Part 3): Balance Sheet Reduction is the Beginning of the Crash and the End of the Bull Market

The Federal Reserve will hold its second FOMC meeting of the year in mid-March, and market expectations for a rate hike at this meeting are exceptionally strong, causing the crypto market to experience continuous decline and remain sluggish. Many investors compare Fed rate hikes to a "bear's ultimate weapon" - as soon as this move is deployed, the market responds with declines, retreating wave after wave.

However, historically speaking, the great bull market of 2017 emerged during a period of continuous Fed rate hikes. If we analyze the full process of the Fed's recent rate hikes in depth, we'll find that rate hikes often amount to just "warm-up exercises" - the Fed's balance sheet reduction is the real "bear's ultimate weapon," a move that draws blood and seals the deal once unleashed.

Last Thursday, the Fed's January FOMC meeting minutes showed: multiple policymakers believe that balance sheet reduction should begin later this year. Although no clear answers were given to questions like "when to start, how fast to proceed, when to stop?" - as soon as the words "balance sheet reduction" were released, the crypto market responded with declines and has been falling since, with accelerated declines appearing yesterday. Historically, every Fed balance sheet reduction has brought about turmoil and even disastrous consequences.

In the third article of our Fed rate hike series, we'll address a core concept of Fed monetary policy: balance sheet reduction. And we'll explain for you: Why balance sheet reduction is the beginning of crashes and the end of bull markets?

The "Dark History" of Fed Balance Sheet Reduction - Does Every Reduction Lead to a Crash?

In 2022, the Fed will primarily do three things: accelerate tapering of bond purchases, raise interest rates by increasing the federal funds rate, and reduce its balance sheet. These three measures progress layer by layer, with each step potentially multiplying the impact.

Now, tapering of bond purchases is nearing completion, and the market has already digested expectations for multiple future Fed rate hikes. This means that among factors that will affect the market going forward, balance sheet reduction will be the key factor.

Historically, the Fed has attempted balance sheet reduction six times before: 1921-1922, 1928-1930, 1937, 1941, 1948-1950, and 2000. Almost every attempt was notorious, with 5 of them ending in economic recession. As shown below:

Historical Fed Balance Sheet Reductions (Source: China Finance)

Looking at the Fed's 6 historical balance sheet reductions, we can see that reductions created significant downward pressure on the economy and markets. Among them, in 1920, the Fed conducted balance sheet reduction 6 times, lasting 1-2 years, with a 15% reduction scale, leading to stock market declines and economic slowdown, shifting from inflation to deflation; in 1930, during the Great Depression, passive balance sheet reduction led to stock market declines and economic collapse; in 1949, after expanding the balance sheet to support the war during WWII, the Fed actively reduced its balance sheet, causing stocks to first decline then rise; in 1969, due to the Marshall Plan, the Fed's passive balance sheet reduction caused small shocks to both stocks and the economy; in 1978-1979, during the second oil crisis, passive balance sheet reduction failed to curb inflation, with both stocks and the economy declining; in 2000 and 2011: after the dot-com bubble burst and 9/11 terrorist attacks, active balance sheet reduction occurred, but since this was the exit of short-term liquidity relief measures from the Fed, the impact was minimal.

Fed balance sheet reduction has a huge impact on the global economy and investment markets, and it's almost always negative. Specifically, global economic growth shows declines - according to World Bank data, the balance sheet reductions in 1960, 1978, and 2000 had relatively small impact on global economic growth in the current period, but in the following 1-2 years, global economic growth showed declines, and US economic growth rates also showed varying degrees of decline during the reduction period.

In terms of global capital flows, after Fed balance sheet reduction, other countries' foreign direct investment (FDI) shows significant declines. For example, during the 2000 reduction, FDI net inflows to high-income countries and low-middle-income countries fell sharply by 47.87% and 8.55% respectively. In contrast, however, US FDI net inflows continued to grow after balance sheet reduction - for example, during the 1978 and 2000 reductions, foreign direct investment into the US grew by 101.72% and 11% respectively. From this perspective, Fed balance sheet reduction can be said to be wielding a harvesting sickle globally.

For global investment markets, basically every reduction, from a long-term perspective, is characterized by major declines - except for the 1949 reduction, the other 5 reductions all caused significant drops in investment market prices like stocks during or after the reduction period. Looking at the most recent reduction, which began in early 2018 and lasted one year, US stocks and other global markets also fell for a year. Bitcoin and the entire crypto market also directly turned from bull to bear, falling for a year, with Bitcoin dropping from nearly $20,000 to over $3,000 - a decline of over 80%. It can be said that the Fed balance sheet reduction cycle is almost synchronized with the decline cycles of stock and other investment markets, which is very concerning.

The Fed has now begun discussing balance sheet reduction matters. Last Thursday's January FOMC meeting minutes also explicitly mentioned the balance sheet reduction topic. If raising rates 2-3 times doesn't have much effect later, the Fed may start balance sheet reduction earlier than expected. Fed Governor Waller mentioned last Friday that "the Fed can begin reducing its balance sheet soon after raising rates." St. Louis Fed President and next year's FOMC voter Bullard also倾向于 starting balance sheet reduction as early as possible. It can be said that this major weapon of balance sheet reduction has been taken out of the Fed's arsenal, just waiting for the right opportunity to be deployed.

The Fed Balance Sheet Reduction Curse - Why Does Every Reduction Bring Disastrous Consequences?

We know that the explosion principle of a "gun-type" atomic bomb is: the initiation controller automatically detonates explosives, rapidly compressing two hemispherical fissile materials into a flat sphere, reaching a supercritical state. The neutron source releases large amounts of neutrons, causing the chain reaction to proceed rapidly, releasing enormous energy in a very short time - this is the hugely destructive atomic bomb explosion.

Analyzing recent Fed rate hikes, we find that in each Fed rate hike cycle, during the initial rate hike stage, the market mostly doesn't show much respect - business as usual. It's not until the balance sheet reduction process begins that the market truly welcomes declines, or even brings disastrous consequences to the world: all investment markets crash, or even trigger major economic recessions.

Fed rate hikes are like the "detonating explosives" of an atomic bomb, while balance sheet reduction is the actual atomic bomb explosion. Why does balance sheet reduction have such power? This can be analyzed from the Fed balance sheet reduction itself and its causes.

Fed balance sheet reduction, simply put, is the act of reducing its own balance sheet scale. The Fed achieves direct recovery of base money by directly selling bonds it holds or stopping reinvestment of maturing bonds. Compared to raising interest rates, this is a more stringent tightening policy. Balance sheet reduction is known as the "nuclear weapon" in the Fed's arsenal, meaning a formal declaration to the world that the US's comprehensive tight monetary policy has arrived.

In early 2020, due to the pandemic impact, the Fed launched an unlimited bond purchase program to boost the market and reduce long-term borrowing costs for businesses and households. To date, the Fed's balance sheet has reached $9 trillion, more than double its previous size. These massive balance sheets mainly consist of US Treasury bonds and MBS securities.

US Treasury bonds are US debt issued by the US Treasury. After the Fed buys US Treasury bonds, it gives the money to the Treasury, which then the government "distributes"; MBS securities are mortgage-backed securities, meaning eligible loans from housing mortgages are pooled together to form a mortgage loan集合体 - that is, the Fed takes on the burden of real estate debt. The former method increases US dollar cash flow by issuing Treasury bonds, while the latter method increases cash flow through lending. Balance sheet reduction can be simply understood as the Fed not only no longer buying bonds, but also starting to sell bonds to recover US dollars.

An important subsequent task for the Fed is to quickly deal with this $9 trillion balance sheet - sell it to take back US dollars, fundamentally reducing US dollar circulation. This is also a key step in recovering US dollars and may fundamentally drain the "water" from the market, at which point almost all markets, including the crypto market, will become dry, and all organisms in the market will face the threat of death.

Looking at the reasons for this Fed balance sheet reduction, continuous rate hikes may not necessarily raise long-term interest rates. Not only can they not curb inflation, but they may also lead to flattening or even inversion of the yield curve. That is, the effectiveness of traditional monetary policy transmission mechanisms has now weakened. Balance sheet reduction is a quantitative tool - if "raising prices" cannot curb economic overheating, then "reducing quantity" will be a more direct choice.

Because this round of inflation was caused by excessive money printing by central banks represented by the Fed - that is, excessive "exogenous money" - the Fed's previous massive balance sheet expansion created flooded liquidity in the market. Now adjusting prices (raising rates) is already difficult to achieve the role of regulating money supply, and a more direct method of controlling money supply is reduction - that is, reducing balance sheet scale. This means that this round of Fed rate hikes may not achieve expected results, and balance sheet reduction will be the final measure, and possibly the measure with more severe market impact.

Therefore, what's truly frightening this year isn't Fed rate hikes, but the Fed beginning to reduce its balance sheet scale. This is the ultimate weapon, the "bear's" atomic bomb.

To summarize, 2022 may be a year of comprehensive tightening. If the Fed begins both rate hikes and balance sheet reduction, we'll enter a period of double tightening. And compared to balance sheet reduction, rate hikes don't yet count as liquidity withdrawal - if we compare rate cuts and QE to stepping on the gas, then rate hikes are equivalent to releasing the gas, and the car will gradually slow down. Balance sheet reduction, however, is truly directly stepping on the brakes. When you step on the brakes, all people and objects in the car will passively stop, or even be thrown about and injured due to inertia.

Although from the Fed's past practices, it always enters a rate hike cycle for a period before beginning balance sheet reduction, this time due to high inflation and economic systemic risks caused by pandemic money printing, the Fed may very well engage in early balance sheet reduction. Compared to rate hikes, balance sheet reduction is truly a nuclear bomb explosion, and its impact on the crypto market could be catastrophic - requiring extreme vigilance.

Disclaimer

This article may contain product-related content not applicable to your region. This article is intended only to provide general information and assumes no responsibility for any factual errors or omissions herein. This article represents only the author's personal views and does not represent OKX's views. This article is not intended to provide any of the following advice, including but not limited to: (i) investment advice or investment recommendations; (ii) offers or solicitations to buy, sell or hold digital assets; or (iii) financial, accounting, legal or tax advice. Holding digital assets (including stablecoins) involves high risk, may fluctuate significantly, and may even become worthless. You should carefully consider whether trading or holding digital assets is suitable for you based on your financial situation. For questions about your specific situation, please consult your legal/tax/investment professional. The information appearing in this article (including market data and statistical information, if any) is for general reference only. Although we have taken all reasonable precautions in preparing these data and charts, we assume no responsibility for any factual errors or omissions expressed herein. © 2025 OKX. This article may be reproduced or distributed in its entirety, or excerpts of 100 words or less from this article may be used, provided such use is non-commercial. Any reproduction or distribution of the entire article must prominently state: "Copyright © 2025 OKX. Used with permission." Permitted excerpts must cite the article name and include attribution, such as "Article Name, [Author Name (if applicable)], © 2025 OKX". Some content may be generated or assisted by artificial intelligence (AI) tools. Derivative works or other uses of this article are not permitted.

Show More

Recommended Reading

2025 KOL Most-Used OKX Products List

In the cryptocurrency industry, professional players' choices are always direct and pure. In 2025, KOLs cast their most genuine votes for industry tools and ecosystem development with a full year of fund investment and time accumulation. We focus on four core questions - "What was the biggest achievement this year?", "Given that achievement, what OKX products did you use most and like best in 2025?", "Why do you like it?", "How did this

January 5, 2026

2026 Investment Outlook: Assets on Chain, Intelligence and Privacy | OKX Annual Review

Three major trends for the future of crypto: asset transformation, entity transformation, and rule transformation. As we approach 2026, bidding farewell to the past four years of infrastructure focus on "building roads," the crypto industry is welcoming a profound paradigm shift. OKX Ventures defines this as the opening of the "Kinetic Finance" era, where the core is no longer how fast the network is, but the flow of on-chain assets and profit-making

December 31, 2025

Voting with Data: Inside 2025's Popular Trading Products | OKX Annual Review

If you only look at market conditions, it's hard to explain the return differences between trading users in 2025. What truly determines returns also depends on account-level operational methods, not just market volatility itself. OKX's annual statement shows that mainstream coins remain the core of fund turnover and return carrying, supporting trading and strategy execution; emerging coins are more used to amplify volatility and provide staged opportunities, but are not stable, long-term return sources. What truly consistently contributes returns,

December 30, 2025

Fusaka in Practice: What Does Ethereum's Latest Upgrade Mean for L2, Nodes, and Users?

Ethereum mainnet has completed the Fusaka fork. From a protocol level, this upgrade mainly includes four parts. The full text presents the core views and frontline experience of three guests in Q&A format: Ahmad (@smartprogrammer) – Nethermind execution client / Ethereum core developer Manu (@manunalepa) – Prysm / Of

December 16, 2025

OKX Research | Why Did RWA Become a Key Narrative in 2025?

RWA (Real World Assets) is becoming the global capital's "new favorite." Simply put, RWA means taking valuable, ownership-bearing things from the real world - such as houses, bonds, stocks and other traditional financial assets, or even assets that are usually difficult to trade directly like artwork, private lending, carbon credits - and moving them onto blockchain to become tradeable, programmable crypto assets. This way, not

November 20, 2025

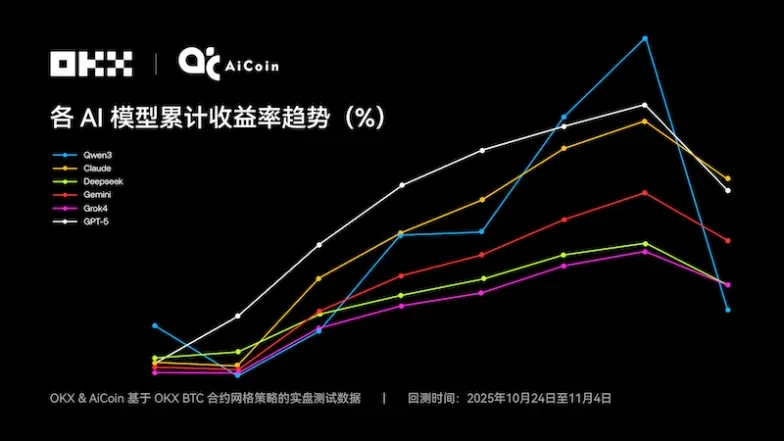

Claude Takes Championship, Truth Behind 6 Major AI Grid Strategy Showdown | OKX & Ai Coin Live Test

Short-term trading champion Qwen3, but is it also king in grid strategies? NOF1's "AI Trading Live Arena" first season finally concluded at 6 AM on November 4, 2025, whetting the appetite of the crypto, tech, and finance circles. But the ending of this "AI IQ public test" was somewhat unexpected - six models with a total principal of $60,000 ended with only 4.3

November 6, 2025