The Business Landscape of Decentralized Derivatives Trading (Part 1)

DYDX-1. 06%

Decentralized derivatives possess most of the advantages of DEXs, such as decentralization, censorship resistance, permissionless nature, and high asset autonomy. With the addition of Layer 2, DEX derivatives also feature orderbooks—the very advantage that CEXs pride themselves on. The combination of DEX derivatives with DeFi and NFTs will unleash infinite possibilities.

It can be said that decentralized derivatives are the culmination of DeFi and the absorber of CEX advantages. However, current DEX derivatives are still in early development, facing issues in product design, trading depth, user habits, and performance. Nevertheless, this does not affect the major trend of DEX derivatives development. This article will provide a comprehensive overview of the current DEX derivatives landscape.

1**,Current Status ofDecentralized Derivatives**

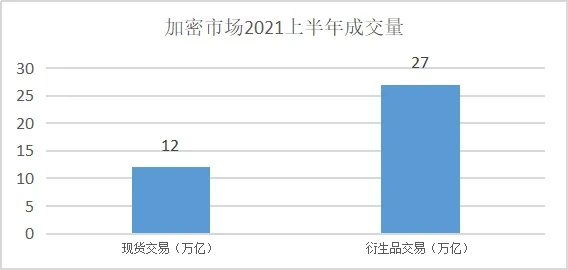

In the previous article "Will Decentralized Derivatives Become Popular?", we mentioned that in the first half of 2021, the top 10 derivatives trading exchanges generated approximately $27 trillion in trading volume, while the top 10 spot trading exchanges reached about $12 trillion—the former being more than double the latter.

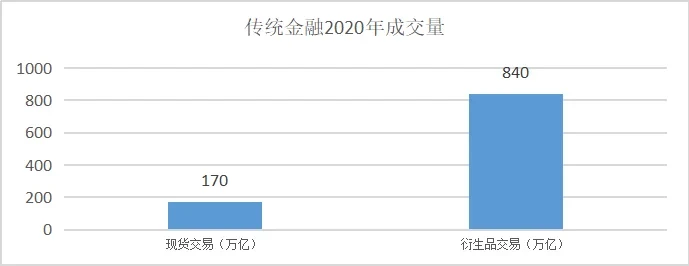

In the traditional financial world, the overall derivatives market's notional value in 2020 was approximately $840 trillion, while the corresponding spot market trading volume for stocks, bonds, and other assets was about $170 trillion. The derivatives market scale is 4-5 times that of spot asset trading.

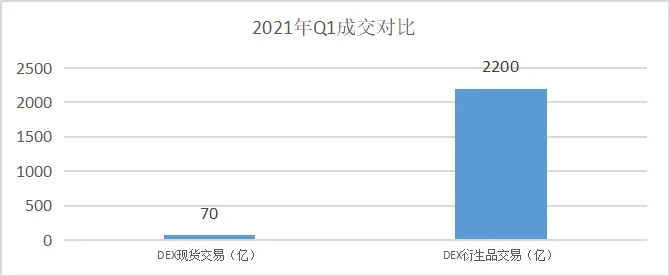

However, in the DEX derivatives market, the situation is恰恰相反. In Q1 2021, decentralized derivatives trading volume was approximately $7 billion, while decentralized spot trading volume in the same period exceeded $220 billion—the latter being 32 times the former.

The above represents the current state of the DEX derivatives market: contrary to the conventional norm of "derivatives trading far exceeding spot trading," but on the other hand, it demonstrates that the DEX derivatives market has tremendous potential. Just as DEXs went from obscurity in early 2020 to explosive growth in the second half, peaking at 40% of total crypto market trading volume, this "feat" could very well occur in the DEX derivatives market.

2**,Two MatchingMethods**for DEX Derivatives Trading**

DEX derivatives can be classified in many ways. By matching method, they can be divided into AMM and orderbook types. By product function, they can be divided into six types: perpetual contracts (Perpetual), options, Layer 2-based stablecoins, interest rate derivatives, binary options, and volatility indices.

By matching method, DEX derivatives are divided into automated market makers (AMM) and orderbooks. Representative projects of the former include Perpetual Protocol, MCDEX, Futureswap, dFuture, Kine Protocol, etc. Representative projects of the latter include dYdX, DerivaDEX, Injective Protocol, Vega Protocol, Serum, etc.

Under the AMM matching trading model, the trader's counterparty is typically the asset pool or stakers. For example, if you stake ETH in Perpetual Protocol's asset pool, you actually become the counterparty to traders. To encourage you to increase staking in the "Pool," the protocol rewards stakers with portions of governance token inflation and trading fees to increase depth, thereby reducing the impact of high leverage on prices. This type of matching mechanism has low tolerance for leverage—Perpetual Protocol supports up to 10x leverage.

Building on AMM, vAMM has evolved. We know that in AMM, stakers need to expose real assets to high leverage, which places investors at high risk. vAMM, called virtual automated market maker, only provides protocol price discovery, while the real assets behind vAMM are stored in smart contract vaults.

Take Perpetual Protocol as an example: a user deposits 100 USDC into a smart contract vault. Assuming a 5x long position is opened, when trading begins, the protocol mints 500 USDC of virtual assets in vAMM. If liquidation occurs, settlement takes place in the smart contract vault, separating the user's real assets from risk.

Products using orderbooks provide investors with a centralized exchange trading experience. For example, the recently popular dYdX employs an orderbook matching mechanism. To improve performance, dYdX uses off-chain orderbooks + on-chain settlement, achieving effects similar to centralized exchanges, and traders don't pay fees for placing and canceling orders. dYdX can support leverage up to 25x.

So, which matching method will the futureDEXderivatives market adopt? The most likely answer is that both are needed.

First, for AMM, as seen on DEXs like Uniswap, Sushiswap, and DoDo, they employ AMM matching methods, allowing users to freely list various token trading pairs—as long as sufficient liquidity is provided, they can open for business. The upcoming Perpetual Protocol v2 Curie version will adopt this model.

On the other hand, orderbooks provide users with a CEX-like trading experience. Taking dYdX as an example, traders get order placement experiences like "market/limit/stop/trailing stop orders." Conversely, in Perpetual Protocol V1, which uses AMM, users can only access market orders.

In reality, designs using both matching methods have already been adopted by DeFi developers. For example, DeGate, a fully L2-based decentralized exchange on Arbitrum, integrated both AMM and orderbook into the product from the outset. An optimistic assessment suggests that AMM + orderbook + Layer 2 will become the standard configuration for next-generation DEXs and the choice for DEX derivatives trading products.

3**, Six Types of DEX Derivatives Trading**

By product type, DEX derivatives can be divided into six categories: perpetual contracts, options, synthetic asset products, interest rate derivatives, binary options, and volatility indices. Among these, products related to perpetual contracts/options are most numerous, and as L2 infrastructure continues to improve, perpetual contract derivatives are showing strong vitality. For example, dYdX based on L2 infrastructure Starkware shows exponential growth in trading volume. On September 20th, dYdX's trading volume exceeded $2.3 billion—90 times the volume from three months ago. Such rapid growth is attributed to dYdX's Layer 2 solution StarkWare.

dYdX trading volume changes, Data source: dydx.exchange

Perpetual contract products mainly include dYdX, Perpetual, Futureswap, MCDEX, Serum, Injective Protocol, DerivaDEX, Kine Protocol.

Currently, dYdX, Perpetual Protocol, and Futureswap are leaders in the centralized derivatives trading space, accounting for over 90% of total market volume. However, with L2 infrastructure like Arbitrum, Optimism, and StarkWare coming online, other products will also have significant growth potential in market share.

Furthermore, as more high-performance L1s in the DeFi ecosystem continue to improve—such as Polygon, Solana, Polkadot, OKTC, Definity, etc.—new competitive landscapes will open up. For example, Kine Protocol simultaneously selects multiple infrastructures (Polygon, ETH, OKTC, etc.), employing on-chain staking + off-chain trading, supporting up to 100x perpetual contracts—making it the highest leverage perpetual contract product in the DEX derivatives world.

Options products mainly include Opyn, Hegic, CHARM, Hedget, Oddz Finance, Permia Finance, Siren, Vega, Auctus, Primitive.Synthetic asset products mainly include Ribbon Finance, Umaproject, Synthetix.Interest rate derivatives mainly include Swivel, Pendle, Element, Sense.Binary options mainly include Thales, Divergence.Volatility indices mainly include Volmex, CVI.

Beyond the above classifications, we must also pay attention to algorithmic stablecoins and stablecoin derivatives based on L2 cross-chain solutions. Currently, Ethereum-compatible sidechains and stablecoin derivatives like xDai provide greater possibilities for DEX derivatives development.

For the three most common categories in DEX derivatives markets—perpetual contracts, options, and synthetic assets—we will select the two most important projects from each category for comparison.

First, let's look at Perpetual and dYdX in perpetual contract products, comparing leverage and collateral, counterparties, risk control, price sources, order types and fees, and user experience.

Perpetual Contracts

Perpetual

dYdX

Maximum Leverage & Collateral

10x USDC

25x USDC

Counterparties

Traders vs Stakers (Peer to Pool)1. 50% of trading fees go to Insurance Fund; 2. 50% of trading fees paid to PERP stakers, 7-day cooling period for fund redemption

Traders vs Market Makers (Peer to Peer)Market makers mainly from DeFi world, such as Wintermute, Amber Group, Wootrade (Kronos), Sixtant, DAT Trading, etc.

Risk Control

1. Insurance Fund and Staking Pool; 2. Emergency shutdown when total assets/total liabilities below 150%

1. Centrally controlled insurance fund; 2. Deleveraging

Price Sources

Benchmark: Virtual Automated Market Maker (VAMM) Index: Chainlink oracle

Benchmark: Orderbook Index: Chainlink oracle

Order Types & Trading Fees

Market orders only; 0.1% trading fee

Market/limit/stop/trailing stop orders; Trading fees range from 0%-0.2% based on volume

User Experience

1. No transfer fees for deposits over $500k (Ethereum users need to transfer funds to xDAI); 2. Contracts easier to understand; 3.Cross-margin

1. No need to transfer assets to Ethereum; 2. Contracts somewhat difficult to understand, requires time to familiarize; 3.Cross-margin

Liquidation Ratio

6.25% margin ratio partial liquidation; 2.5% margin ratio full liquidation

3% margin ratio liquidation

Data source: A&T Capital

Next, let's look at Hegic V8888 (V8888 represents the latest version) and Opyn in options products, comparing supported products, liquidity sources, risk control, price sources, order types and fees, user experience, and capital efficiency.

Options

Hegic V8888

Opyn

Current Products

Buy/sell wBTC/ETH call options (cash-only), under 90 days, American-style, automatically exercising cash-settled options

Buy/sell wBTC/ETH call options (cash-only), under 120 days, European-style, automatically exercising cash-settled options

Liquidity Sources

Traders vs Stakers (Peer to Pool)Deposit as option writers to receive premiums

Traders vs Market Makers (Peer to Peer)

Risk Control

Staking pool receives settlement fees and trading fees

Sellers must maintain minimum collateral, e.g., selling 1 ETH call option

Price Sources

Chainlink oracle

Chainlink oracle

Order Types/Fees

Strike options only; LPs receive settlement fees included in premiums, option buyers pay 10%-30% of total premium

Orderbook; Currently no trading fees

User Experience

1. Currently zero fees only for large trades, e.g., 1w BTC 2. Easier to understand

1. Professional orderbook harder to understand 2. Only suitable for institutions

Capital Efficiency

Issue staking rate set at 50%

Partial collateralization at 40% collateral rate

Data source: A&T Capital

Finally, let's look at Synthetix and UMA in synthetic asset products, comparing supported products, counterparties, risk control, price sources, order types and fees, user experience, and capital efficiency.

Synthetic Assets

Synthetix

UMA

Current Products

Long (sBTC) or short (iBTC) crypto assets/forex/stocks/commodities

Options, zero-coupon bonds, etc.

Counterparties

Traders vs Stakers (Peer to Pool)Stake SNX, receive trading fees and SNX inflation rewards

Traders vs Market Makers (Peer to Peer)

Risk Control

1. Staking pool; 2. Freeze and suspend trading

Platform has no risk as it only provides templates for creating derivatives

Price Sources

Chainlink oracle

Chainlink oracle UMA DVM resolves liquidation disputes

Fees

0.1%-1%, typically 0.3%

—

User Experience

1. Too many sub-apps increase complexity 2. Difficult to understand and use

1. Difficult to understand, high barrier to creating trading templates 2. Provides various derivative tools

Liquidation Ratio

L2 initial margin 1000%; Margin below 200% for 3 days triggers liquidation

125% collateral ratio

Data source: A&T Capital

Due to space limitations, this article currently presents the first three parts. The next four parts will be published next week (September 29). Stay tuned. Note: "The Business Landscape of Decentralized Derivatives" is planned to have seven parts total: 1) Current status of decentralized derivatives trading, 2) Two matching methods for DEX derivatives trading, 3) Six types of DEX derivatives trading, 4) DEX derivatives business landscape, 5) When Layer 2 meets DEX derivatives, 6) The possibilities of decentralized derivatives, 7) What problems do decentralized derivatives face?

Disclaimer

This article may contain content about products not available in your region. This article is intended to provide general information only and does not take responsibility for any factual errors or omissions herein. This article represents only the author's personal views and not those of OKX. This article is not intended to provide any advice, including but not limited to: (i) investment advice or investment recommendations; (ii) offers or solicitations to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. Holding digital assets (including stablecoins) involves high risk, may fluctuate significantly, and may even become worthless. You should carefully consider whether trading or holding digital assets is suitable for you based on your financial situation. For questions about your specific situation, please consult your legal/tax/investment professional. Information appearing in this article (including market data and statistics, if any) is for general reference only. While we have taken all reasonable precautions in preparing these data and charts, we accept no responsibility for any factual errors or omissions expressed herein. © 2025 OKX. This article may be reproduced or distributed in its entirety, or excerpts of 100 words or less may be used, provided such use is non-commercial. Any reproduction or distribution of the entire article must prominently state: "Copyright © 2025 OKX. Used with permission." Permitted excerpts must cite the article name and include attribution, e.g., "Article Name, [Author Name (if applicable)], © 2025 OKX". Some content may be generated or assisted by artificial intelligence (AI) tools. Derivative works or other uses of this article are not permitted.

Show More

Recommended Reading

OKX Pay: Opening a New Era of Next-Generation Crypto Payments

The choice of tens of millions of users. Register on OKX to enjoy the ultimate trading experience and diverse wealth management products. A letter from OKX CEO Star: Today, we officially launch the first version of OKX Pay to over 100 million global users. As the industry's first payment application to truly achieve non-custodial and compliant integration, OKX Pay will be embedded within the OKX App, currently available in select markets, with full rollout expected within months

March 22, 2026

New Chapter: Building Next-Generation Financial Infrastructure Together

The partnership between OKX and Intercontinental Exchange (ICE) is an important moment for OKX and equally significant for the evolution of the entire digital assets market. ICE establishes and operates the world's most important financial infrastructure, including the New York Stock Exchange and global derivatives and clearing platforms. ICE's strategic investment in OKX and joining our board reflects both parties' shared belief—digital assets technology will transform financial markets

March 10, 2026

Tribute to Another Year of Forging Ahead

As CEO of OKX and a builder who remains true to our original mission, I proudly look back on OKX's remarkable growth and progress this year. Despite many challenges, 2024 has been a year of focus, innovation, and resilience. We have not only expanded and optimized our products but also made significant progress in launching transparent and compliant localized businesses, while further strengthening our global management team. Notably, after experiencing

January 29, 2026

2025: Steady Progress Toward Financial Freedom Together

— Year-end letter from OKX Founder and CEO Star to global users "Financial freedom" is often misunderstood. It doesn't mean absence of rules, but rather having the right to choose within the framework of rules—and when the system is truly tested, it remains reliable and effective. This is exactly what we focused on throughout 2025. First, I want to extend sincere gratitude to our global clients, partners, and regulatory bodies

January 16, 2026

OKX Officially Launches in Germany and Poland

Author: Erald Ghoos, CEO of OKX Europe Today is significant for OKX—and for crypto users across Europe. We have officially launched fully compliant centralized cryptocurrency trading platforms in Germany and Poland! For us, this is more than just geographic expansion—it's a commitment to building the cryptocurrency future the right way: secure, transparent, and meeting local needs. If you're in Germany

October 21, 2025

Partnership Expanded! OKX Partners with Standard Chartered to Expand European Market

On October 15, OKX Europe CEO Erald Ghoos stated that OKX is expanding its strategic partnership with Standard Chartered to the European Economic Area (EEA). Earlier this year, OKX first partnered with Standard Chartered in the UAE to launch the collateral mirroring program—a

October 15, 2025