The Business Landscape of Decentralized Derivatives Trading (Part 2)

The previous article "The Business Landscape of Decentralized Derivatives Trading (Part 1)" introduced the current state, classification, and comparison of DEX derivatives, noting that current DEX derivatives trading volume is relatively low with significant growth potential in the future. DEX derivatives trading is categorized by type into perpetual contracts, options, synthetic asset products, interest rate derivatives, binary options, and volatility indices, and by matching form into AMM and Order Book types. This second half will introduce the remaining three sections.

4. The Business Landscape of DEX Derivatives Trading

Derivatives trading represents a more advanced form of commercial activity and is also the more popular trading form in mainstream global trading markets. In traditional finance, derivatives trading is conducted in specialized trading institutions, strictly separated from spot markets such as stocks, bonds, and foreign exchange.

For example, LaSalle Street in Chicago, USA, gathers the vast majority of futures and derivatives trading in the United States. LaSalle Street to the derivatives market is what Wall Street is to the US securities market, contributing the majority of global derivatives market trading volume. The renowned Chicago Mercantile Exchange (CME) and Chicago Board Options Exchange (CBOE), two of the world's largest options exchanges, are located here.

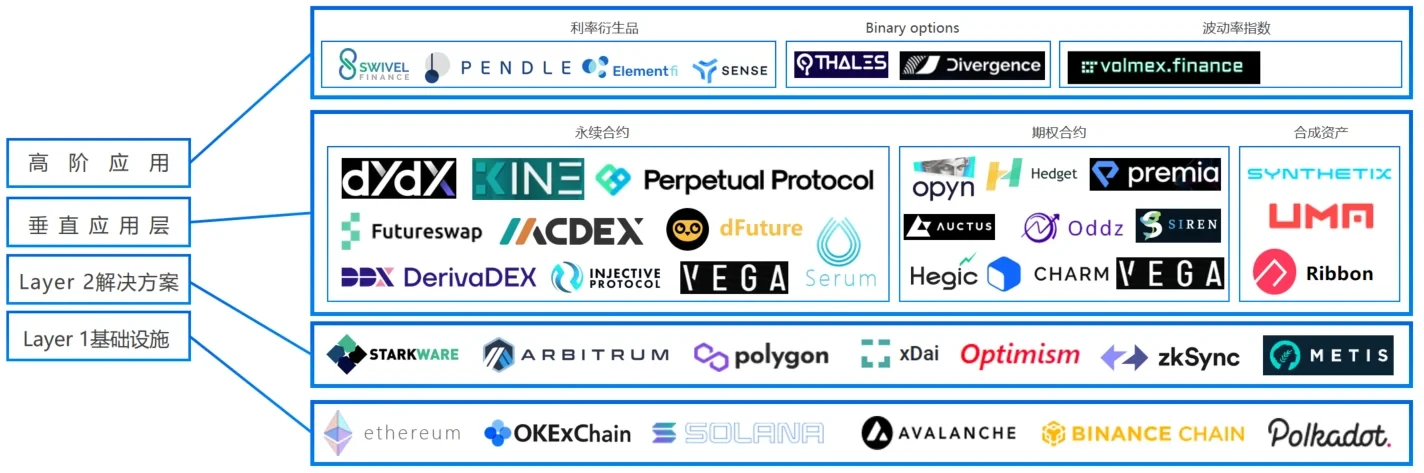

In the future, derivatives trading markets will be strictly separated from other trading categories in the DeFi market, making it necessary to classify and discuss the business logic and commercial landscape of DEX derivatives trading. Currently, the architecture of DEX derivatives trading can be divided into 4 levels, from bottom to top: L1 infrastructure, various Layer 2 solutions, vertical applications, and advanced derivatives trading.

First, let's look at L1**** infrastructure.

DEX derivatives infrastructure consists of Ethereum and other high-performance L1s (OKT Chain/Solana/Avalanche, etc.). Currently, most products choose to build trading on Ethereum-based Layer 2, such as the most mainstream dYdX, Synthetix, MCDEX, Perpetual, etc. However, some products also choose to build business across multiple high-performance L1 and Layer 2 network architectures. For example, Kine Protocol chooses to simultaneously cross-chain ETH, Polygon, OKTC, BSC, Heco, adopting on-chain staking + off-chain trading form, achieving 0 gas fees, 0 slippage long/short trading, reaching CEX user experience.

In addition, the Order Book-based perpetual contract product Injective has taken a different approach, choosing to build an independent decentralized Layer 2 network based on Cosmos technology architecture. This network consists of three parts: Injective Blockchain, Injective DEX, and Injective Bridge. The Injective DEX protocol responsible for trading is built upon this network.

However, with the continuous improvement of high-performance L1 infrastructure, building products directly on high-performance L1s may be a good choice. For example, Serum is directly built on Solana as a perpetual contract-type product.

Next are Layer 2**** solutions.

With the continuous improvement of Ethereum Layer 2, infinite possibilities have been opened up for DEX derivatives trading. Its significance is no less than Axie launching on Ronin, because derivatives trading has extremely high requirements for infrastructure performance, especially for Order Book-matched derivatives.

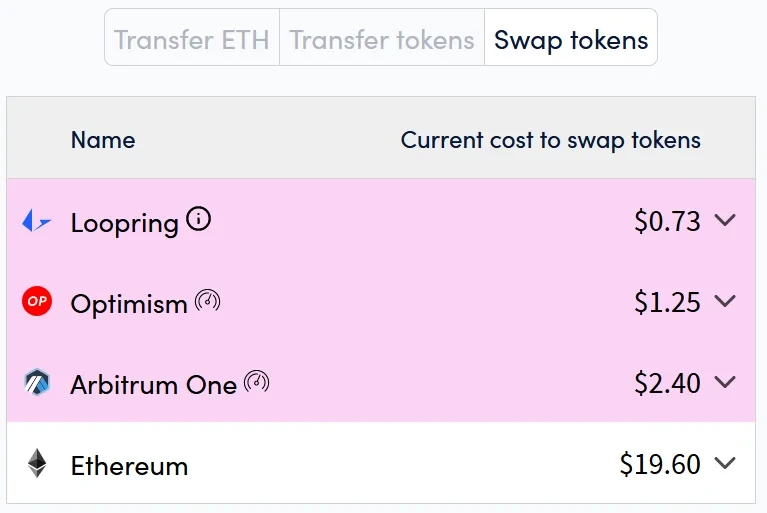

Currently mainstream Ethereum Layer 2 solutions include zkSync, Starkware, Optimism, Arbitrum, Immutable X, Metis, Hermez, with Polygon as a sidechain. Although the Starkware network is still some time away from true openness, it has already attracted excellent projects such as dYdX, DiversiFi, and Sorare. MCDEX, Futureswap v3, Perpetual, and others choose to run on Arbitrum, while Synthetix and others choose to cooperate with Optimism. Currently, various Layer 2 infrastructures are still being improved, but there is still a significant improvement in DeFi transaction fees. As shown in the figure below, a Swap transaction fee based on Arbitrum One is only 12% of L1.

Data source:https://l2fees.info/

Then comes the vertical application part.

The vertical application part includes three categories: perpetual contracts, option contracts, and synthetic assets, and is the most critical business part of DEX derivatives. Perpetual contract products mainly include dYdX, Perpetual, Futureswap, MCDEX, Serum, Injective Protocol, DerivaDEX, Kine Protocol. Option products mainly include Opyn, Hegic, CHARM, Hedget, Oddz Finance, Permia Finance, Siren, Vega, Auctus, Primitive. Synthetic asset products mainly include Ribbon Finance, Umaproject, Synthetix.

Among these, perpetual contract products are the focus.

Since 2021, decentralized perpetual contracts have progressed rapidly. Perpetual Protocol, which initially ran on xDai, became the first decentralized perpetual contract trading platform with a daily trading volume exceeding $100 million in February of this year, once accounting for over 80% of decentralized derivatives trading volume. Subsequently, the upgraded Perpetual Protocol v2 and Perpetual Protocol v3 versions chose to launch on Arbitrum. After September this year, with the gradual improvement of Layer 2 and the launch of dYdX trading mining strategy, trading volume caught up from behind, with daily trading volume reaching a historical high of $9.1 billion on September 17.

It took Uniswap more than two months for its daily trading volume to surpass the world's largest compliant exchange Coinbase. How long will it take for DEX derivatives exchange trading volume to surpass the largest CEX? Let's wait and see.

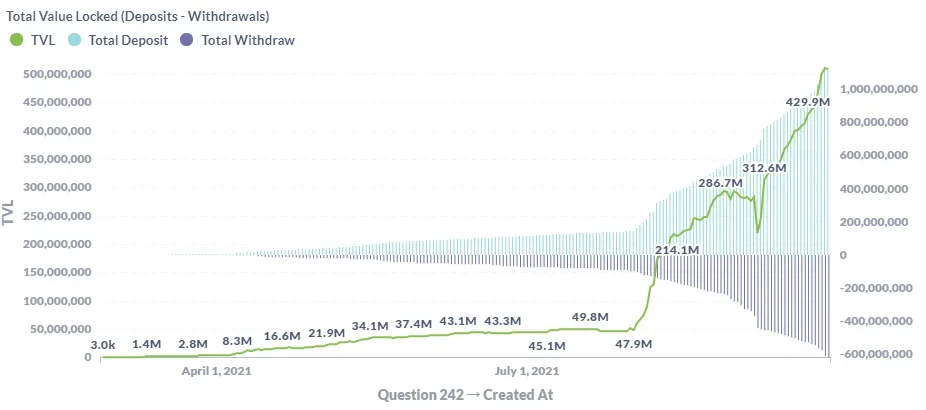

For derivatives trading, how to improve liquidity is the most important issue second only to security. dYdX incentivizes liquidity from multiple dimensions including trading, positions, providing liquidity, USDC staking, and market maker zero-interest unsecured lending. For example, dYdX rewards users based on their trading fees and open interest, which accounts for 25% of dYdX's total. In addition, to improve trading depth, dYdX has also approved Wintermute, Amber Group, Wootrade (Kronos), Sixtant, and DAT Trading to participate in market making. Under these numerous initiatives, as of September 27, CoinGecko data shows that dYdX's 24-hour trading volume exceeded $6.5 billion, already surpassing the sum of all DEXs. dYdX's TVL also repeatedly reached new highs, reaching a historical high of $526 million.

Data source:https://metabase.dydx.exchange/public/dashboard/5fa0ea31-27f7-4cd2-8bb0-bc24473ccaa3

Finally, let's look at advanced applications.

Advanced applications of decentralized derivatives include interest rate derivatives (Swivel, Pendle, Element, Sense), binary options (Thales, Divergence), and volatility indices (Volmex, CVI).

So what can these derivatives bring to the crypto industry?

Taking interest rate derivatives as an example, in traditional stock trading markets, holding stocks and receiving stock dividends are tightly bundled. However, if DeFi thinking is introduced, stocks and dividends can be separated. By issuing principal tokens and yield tokens, the former represents users' locked principal positions, while the latter can claim the base yield rate of assets deposited on the platform, achieving complete separation of principal and yield rate, circulating separately, and increasing capital utilization.

For example, Pendle users can choose to lock deposit certificates from deposit protocols such as Aave and Compound in Pendle's smart contracts, obtaining OT (Ownership Token representing users' claim rights to collateral) and XYT (tokens representing future yield). Sellers can sell XYT on DEX, thereby locking in yield and achieving fixed-rate deposits; or they can put them in liquidity pools to provide liquidity and earn Pendle tokens. Buyers, on the other hand, use relatively small principal to purchase the yield rights of the corresponding OT for a certain future period.

Taking Element Finance as another example, in this protocol users can divide base assets (such as ETH, BTC, USDC, etc.) into two parts—Principal Token (PT) and Yield Token (YT). Suppose investor Xiao Ming holds 1000 USDC and deposits them into Element Finance, he can get 1000 pt USDC and 1000 yt USDC. From then on, Xiao Ming can control and trade principal and yield as two different tokens, PT and YT.

So, can Xiao Ming sell 1000 pt USDC and only hold yt USDC? Of course, Xiao Ming can sell pt USDC to Xiao Zhang, while the held YT continues to earn interest. At this time, Xiao Zhang can operate the held pt USDC again, for example, exchanging it for USDC and repeating Xiao Ming's actions.

In summary, advanced DEX derivatives gameplay will awaken more advanced financial derivatives and push DeFi to new heights.

5. The Imagination Space of Decentralized Derivatives

DEX derivatives will bring at least three aspects of imagination space: DEX derivatives combined with DeFi/NFT, DEX derivatives trading combined with traditional financial markets, and the trading growth of the DEX derivatives market itself.

First, DEX derivatives trading combined with DeFi/NFT will unleash infinite imagination.

Combinations are based on mechanism design needs and market demand. In terms of mechanism design, taking the "marriage" of Perpetual Protocol and Uniswap v3 as an example, after the protocol upgraded to V2 Curie version, it chose to deploy the protocol on Arbitrum. This version executes its perpetual contract trading in Uniswap v3's concentrated liquidity pool, giving Perpetual Protocol stronger scalability, liquidity aggregation, and free market creation characteristics. More importantly, such a "marriage" inadvertently facilitated another important model—"Cross Margining". Currently, the V2 Curie version has reached the first stage, launching Uniswap V3 concentrated liquidity and market maker strategies on Arbitrum.

In terms of market demand, as everyone knows, during the NFT bull market, one sky-high NFT work after another was born. Beeple's "Everydays: The First 5000 Days" sold for $69 million, followed by Crypto Punk #7804 sold for 4200 ETH (approximately $7.57 million), and later Crypto Punk #7523 was acquired by Draft Kings major shareholder Shalom Meckenzie for $11.8 million...

The NFT craze will inevitably continue in the future, but excessively high prices have also led to extremely poor liquidity in this category. If these NFTs could be tokenized, their liquidity would greatly increase. They could even be combined with DEX derivatives trading to include NFT forward prices in trading, which could also partially solve the problem of poor NFT liquidity.

In addition, DEX**** derivatives trading will also have an impact on traditional derivatives markets.

Currently, hundreds of exchanges worldwide, including CEX/DEX, mainly focus on crypto asset trading. In the future, will DEX derivatives exchanges be able to include more traditional assets? They could be soybeans, wheat, corn, ethanol, thermal coal, beef and mutton, crude oil, metals, etc. Eventually, a certain DEX derivatives exchange could develop into a giant like the Chicago Mercantile Exchange to meet global decentralized hedging needs for various underlying assets. In addition, compared to the centralized finance world's Monday-to-Friday trading, DeFi's 24-hour trading, 365 days a year, can better meet traders' needs.

Finally, in terms of market cap growth.

According to the rule that "derivatives trading volume in mature financial markets is generally several times that of spot trading volume," for example, the overall notional value of the derivatives market in 2020 was approximately $840 trillion, while the corresponding spot market trading scale for stocks, bonds, etc. was approximately $170 trillion. The derivatives market size is 4-5 times that of spot asset trading volume.

Currently, DEX derivatives daily trading volume is about $3 billion, and DEX spot trading volume is about $220 billion. From this, it is believed that normal DEX derivatives trading should be $900 billion, meaning there is still 300x upside potential in terms of trading volume. In the future, with Ethereum Layer 2 and numerous high-performance L1 support, this goal may be achieved.

6. What Problems Do Decentralized Derivatives Face?

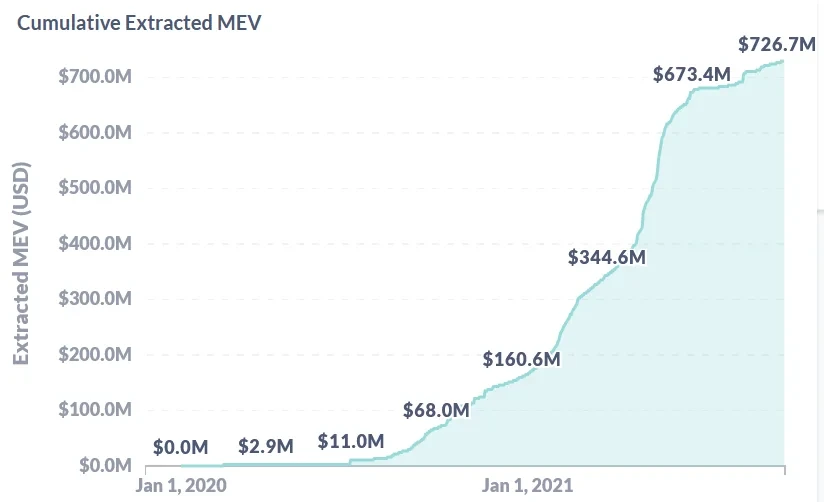

In the context of Ethereum L1, the professional expression for miner front-running is Miner Extractable Value (MEV), which refers to the additional profit miners can obtain beyond block rewards and transaction fees by auctioning the transaction ordering in their mined blocks. As of the end of September, Ethereum miners' cumulative extractable value reached as high as $726 million. This has spawned various forms of arbitrage robots, including front-running robots, back-running robots, liquidation robots... Ordinary traders have to pay for this.

Data source:https://explore.flashbots.net/

Of course, the most thorough solution to this problem is ETH transitioning to PoS, completely eliminating Ethereum miners. However, since ETH 2.0 full implementation will still take several years, before that, the Ethereum ecosystem is also responding to miner extractable value through various clever methods. Projects such as Eden Network and Flashbots have each given solutions to this problem, to some extent solving the miner extractable value problem.

However, in DEX derivatives, everything has changed. This is because, compared to simple token swaps, derivatives trading is much more complex, involving a series of risk management, margin trading, liquidation mechanisms, and stable price feeding mechanisms. However, with Ethereum Layer 2 gradually coming online, due to its higher throughput, Layer 2 can achieve oracle low latency, which may prevent front-running.

In addition, DEX**** derivatives have extremely high requirements for oracles.

In product settings, products including mainstream perpetual contracts (Perpetual/dYdX), options (Hegic/Opyn), and synthetic assets (Synthetix/UMA) all use Chainlink oracles as price sources. This poses no problem in spot trading markets like Uniswap, but because derivatives trading often involves tens of times leverage, price sensitivity increases by orders of magnitude, requiring oracles like Chainlink to have extremely high reliability and stability.

Finally, there is the application of cross-margining mechanisms. In mid-July, Multicoin Capital Managing Partner Kyle Samani proposed through a series of tweets that in derivatives trading, cross margining is everything. Compared to the widespread adoption of this mechanism by centralized exchanges, currently only a few such as Perpetual and dYdX in the DEX derivatives space are launching this mechanism, which also illustrates from the side that DEX derivatives markets still have a long way to go in competing with centralized exchanges.

In summary, although DEX derivatives currently have various problems, I believe that with the efforts of many wise minds in the crypto community, all problems will eventually be solved, and we will welcome a new era of DEX derivatives.

Disclaimer

This article may contain content about products that are not available in your region. This article is intended to provide general information only and does not take responsibility for any factual errors or omissions therein. This article represents only the author's personal views and does not represent the views of OKX. This article is not intended to provide any advice, including but not limited to: (i) investment advice or investment recommendations; (ii) offers or solicitations to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. Holding digital assets (including stablecoins) involves high risk, may fluctuate significantly, and may even become worthless. You should carefully consider whether trading or holding digital assets is suitable for you based on your financial situation. For questions about your specific situation, please consult your legal/tax/investment professional. The information appearing in this article (including market data and statistics, if any) is for general reference only. While we have taken all reasonable precautions in preparing these data and charts, we accept no responsibility for any factual errors or omissions expressed herein. © 2025 OKX. This article may be reproduced or distributed in its entirety, or excerpts of 100 words or less from this article may be used, provided such use is non-commercial. Any reproduction or distribution of the entire article must prominently state: "© 2025 OKX, used with permission." Permitted excerpts must cite the article name and include attribution, for example "Article Name, [Author Name (if applicable)], © 2025 OKX". Some content may be generated or assisted by artificial intelligence (AI) tools. Derivative works or other uses of this article are not permitted.

Show More

Recommended Reading

OKX Pay: Opening a New Era of Next-Generation Crypto Payments

The choice of tens of millions of users. Register with OKX and enjoy ultimate trading experience and diverse wealth management products. A letter from OKX CEO Star: Today, we officially launch the first version of OKX Pay to over 100 million global users. As the industry's first payment application that truly achieves non-custodial and compliant integration, OKX Pay will be embedded in the OKX App, currently open to some markets, and expected to fully launch within a few months

March 22, 2026

New Chapter: Building Next-Generation Financial Infrastructure Together

The partnership between OKX and Intercontinental Exchange (ICE) is an important moment for OKX and equally significant for the evolution of the entire digital asset market. ICE establishes and operates some of the world's most important financial infrastructure, including the New York Stock Exchange and global derivatives and clearing platforms. This investment by ICE in OKX and joining our board reflects our shared belief—that digital asset technology will be in the financial markets

March 10, 2026

Tribute to Another Year of Forging Ahead

As CEO of OKX and a builder who stays true to our original vision, I am proud to look back on the remarkable growth and progress OKX has achieved this year. Despite numerous challenges, 2024 has been a year of focus, innovation, and resilience. We have not only expanded and optimized our products but also made important progress in launching transparent and compliant localized operations, while further strengthening our global management team. Notably, after experiencing

January 29, 2026

2025: Steady Progress Toward Financial Freedom Together

— Annual Letter from OKX Founder and CEO Star to Global Users "Financial freedom" is often misunderstood. It doesn't mean no rules, but rather having the right to choose within the framework of rules—and when the system is truly tested, it remains reliable and effective. This is exactly what we focused on throughout 2025. First, I would like to extend my sincere gratitude to our global clients, partners, and regulatory authorities

January 16, 2026

OKX Officially Launches in Germany and Poland

Author: Erald Ghoos, CEO of OKX Europe Today is a significant day for OKX—and for crypto users across Europe. We have officially launched our fully compliant centralized cryptocurrency trading platform in Germany and Poland! For us, this is not just a geographic expansion, but a commitment to building the cryptocurrency future the right way: secure, transparent, and meeting local needs. If you are in Germany

October 21, 2025

Partnership Upgrade! OKX Partners with Standard Chartered to Expand European Market

On October 15, OKX Europe CEO Erald Ghoos stated that OKX is expanding its strategic partnership with Standard Chartered to the European Economic Area (EEA). Earlier this year, OKX first partnered with Standard Chartered in the UAE to launch the collateral mirroring program—a

October 15, 2025