Will Decentralized Derivatives Trading Take Off?

DYDX-1. 06%

Constrained by issues such as network performance, risk control, capital efficiency, and liquidity, decentralized derivatives trading has not yet gone mainstream despite years of exploration.

However, this does not mean it has stagnated. Just two years ago, no one could have imagined that DEX trading volume would reach 40% of CEX volume, and as early as July 2020, Uniswap's trading volume alone exceeded that of the world's most renowned CEX.

With the launch of numerous outstanding Layer 2 solutions (Optimism, Arbitrum, Metis, etc.), the issues plaguing decentralized derivatives trading — miner front-running, high fees, low performance — will gradually be alleviated. At that time, we will see a brand-new crypto derivatives market.

So, what is the current state of the decentralized derivatives trading market? What dramatic changes will occur in crypto derivatives trading as Ethereum Layer 2 infrastructure continues to improve? And what will be the relationship between decentralized derivatives trading and centralized derivatives markets?

1. Current State of Decentralized Derivatives Trading

In general, in mature trading markets, derivatives trading volume far exceeds spot trading volume.

For example, the latest data shows that in just the first half of 2021, the top 10 crypto derivatives exchanges generated approximately $27 trillion in trading volume, while the top 10 spot exchanges was about $12 trillion — the former being more than twice the latter.

Additionally, according to the latest data from Coingecko, the world's top seven derivatives exchanges are OKXOKEX, Binance, Huobi, Bybit, FTX, Bitget, and BitMEX, among which OKXOKX recently maintained daily spot trading volume around $9.6 billion, while derivatives trading volume was approximately $30 billion — the latter being 3.1 times the former.

This clearly demonstrates that derivatives trading volume far exceeds spot trading volume, a trend that also holds true in traditional financial markets.

In the traditional financial world, financial derivatives include but are not limited to forward contracts, options contracts, and other contract forms. The underlying assets behind these contracts include stocks, currencies, commodities, etc. According to 2020 derivatives statistics, the overall nominal value of the derivatives market in 2020 was approximately $840 trillion, while the trading scale of spot markets such as stocks and bonds was about $170 trillion — the derivatives market being 4-5 times the size of spot asset trading volume.

However, in the decentralized derivatives market, the situation is precisely the opposite. On one hand, compared to the centralized derivatives market, decentralized derivatives trading appears insignificant. On the other hand, decentralized derivatives trading volume also far falls short of DEX spot trading volume.

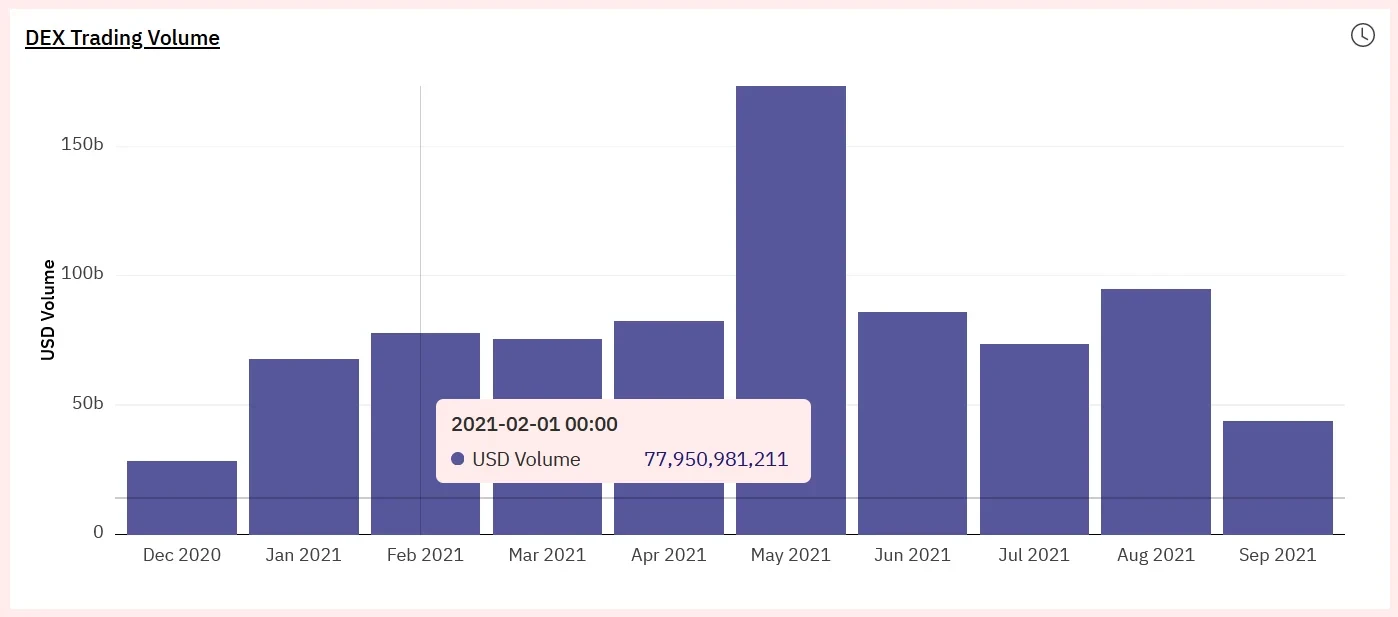

First, let's look at the comparison data between decentralized spot trading and decentralized derivatives. Taking Q1 2021 market data as an example, decentralized derivatives trading volume was approximately $7 billion, while decentralized spot trading volume in the same period exceeded $220 billion — the latter being 32 times the former. This stands in stark contrast to the traditional norm where "derivatives trading far exceeds spot trading."

Data source: dune. xyz

Additionally, the trading volume of the decentralized derivatives market also pales in comparison to the centralized derivatives market. In Q1 2021, centralized perpetual contract trading exceeded $14 trillion — 2000 times the $7 billion decentralized derivatives trading volume in the same period.

At the DEX level, Uniswap V2 and V3's total 24-hour trading volume was $1.25 billion, while decentralized contract exchanges represented by Perpetual Protocol had 24-hour trading volume of $96 million — spot trading volume being 13 times derivatives trading volume in the decentralized world.

Through the above data comparison, we can see that the decentralized derivatives market still has a long way to go.

Looking back at the development of DEXs like Uniswap, under the AMM mechanism, DEX spot markets captured 40% of the crypto trading market share in less than half a year, with a thriving overall ecosystem. So, what is hindering the development of decentralized derivatives trading? Why haven't decentralized derivatives taken off yet?

2. Why Haven't Decentralized Derivatives Taken Off Yet?

On the path of DEX development, various issues have been encountered, such as high barriers, few listed tokens with poor depth, high fees, and low efficiency — general problems, as well as deeper issues like impermanent loss in AMM pools and miner front-running.

The former can be addressed through user education, trading expansion, and other means, while the latter requires deep-level innovation from a mechanism perspective. Taking miner front-running as an example, the professional expression for this phenomenon is Miner Extractable Value (MEV), which refers to the additional profit miners can obtain beyond block rewards and trading fees by auctioning the ordering of transactions in their mined blocks. This has given rise to various forms of arbitrage bots, including front-running bots, back-running bots, liquidation bots... Ordinary traders have to pay for this.

Of course, the most thorough solution to this problem is ETH transitioning to PoS, completely eliminating Ethereum miners. However, since ETH 2.0 full implementation will still take several years, before that, the Ethereum ecosystem has also adopted various clever methods to deal with miner extractable value. Projects like Eden Network and Flashbots have each provided solutions to this problem, largely resolving the miner extractable value issue.

In summary, various problems exist in the DEX spot trading market, and corresponding solutions can be found — even for deep-seated issues like miner extractable value brought about by Ethereum's native mechanisms.

However, decentralized derivatives are not so fortunate.

First, compared to simple token swaps, derivatives trading is much more complex, involving a series of risk management, margin trading, liquidation mechanisms, and stable price feeding mechanisms.

Second, in derivatives markets, the miner transaction front-running problem is even more difficult to solve. For example, among Synthetix's latest 50 improvement proposals, 25% are addressing the front-running problem. As early as 2019, in a miner front-running incident, a bot extracted 11 billion sETH from a failed price feed! Fortunately, the Synthetix team discovered and froze the protocol in time, avoiding worse outcomes and pulling Synthetix back from the brink of destruction.

However, this does not mean decentralized derivatives trading has no future. On the contrary, as Ethereum Layer 2 infrastructure continues to improve, the previous issues of high fees, low performance, and front-running can all be resolved.

Currently, different decentralized derivatives platforms have adopted different scaling solutions. The more mature contract trading platform Perpetual Protocol selected the sidechain solution xDai, while dYdX selected Stark Ex developed by the Israeli development team StarkWare as scaling infrastructure. The well-known DeFi project Synthetix uses the Layer 2 solution Optimism, which is based on Optimistic Rollup, for scaling.

With the continuous performance improvement of scaling solutions like Arbitrum, Optimism, StarkWare, Zksync, and Metis, after ensuring real-time transaction confirmability, both miner front-running and performance issues will be readily solved.

What will be the relationship between decentralized derivatives trading and centralized derivatives trading in the future?

3**, Complementary or Mutually Destructive? **

Some might believe that as decentralized derivatives trading gradually improves, it will eventually replace the derivatives market share of centralized exchanges. Will this speculation materialize?

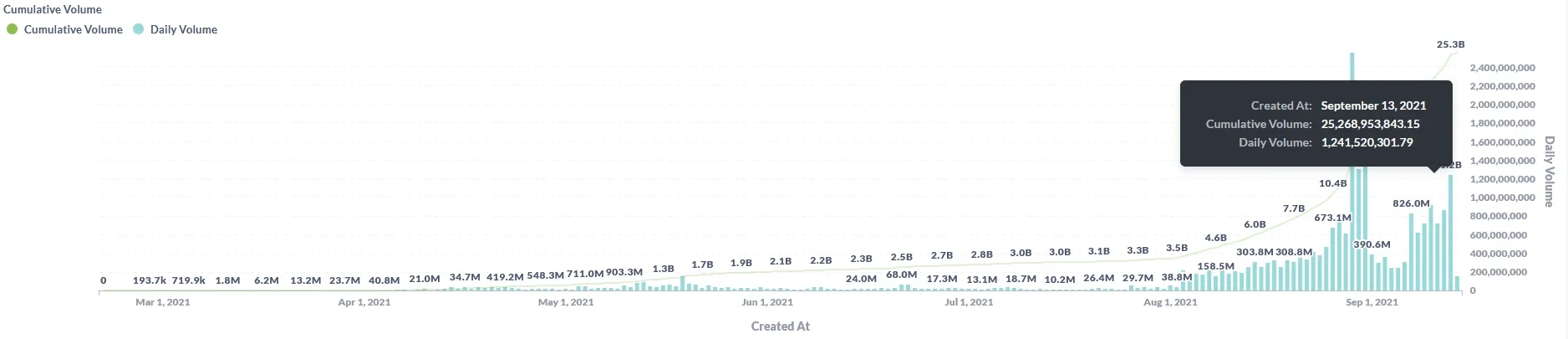

In fact, the current decentralized derivatives market share is rapidly rising. On September 13th, dYdX's trading volume exceeded $1.2 billion — 40 times its volume three months prior. Such rapid growth is attributed to dYdX's Layer 2 solution StarkWare. Additionally, we know that Perpetual Protocol V1 utilized xDAI sidechain scaling, while Perpetual Protocol V2 and V3 have selected Arbitrum to establish perpetual contracts.

Data source: metabase. dydx. exchange

Decentralized derivatives exchanges also offer advantages such as decentralized asset custody, more open autonomous systems, more public and transparent governance systems, and anonymity that centralized exchanges do not possess.

Does this mean that decentralized derivatives trading will replace centralized derivatives exchanges?

Of course not.

Just as when we discussed whether DEXs would replace CEXs due to their many decentralization advantages, we never imagined that the US SEC would loudly and prominently investigate Uniswap's actual development and control team, Uniswap Labs, in early September. And two months prior, in July, Uniswap Labs restricted the trading of 129 tokenized stocks, mirror stocks, options, and derivatives tokens on its protocol frontend, citing a "changing regulatory environment."

Therefore, so-called decentralization is only relative. Even though dYdX's current daily trading volume has reached over $1.2 billion, the protocol's control rights have not been opened to the community. You can consider dYdX to still be a centralized exchange so far.

Decentralized derivatives trading still faces other issues.

First, the liquidation mechanism is a major issue facing both decentralized and centralized exchanges. Compared to the powerful processing capabilities of centralized exchanges, decentralized platforms need to handle various issues brought about by on-chain congestion during sharp price fluctuations.

Second, decentralized derivatives exchanges also face capital efficiency issues. The core demand for traders participating in derivatives trading is the ability to conduct margin trading with added leverage. However, the over-collateralization mechanism introduced by some synthetic asset projects once again limits the efficient use of funds. For example, derivatives exchanges like Synthetix require over-collateralization with a collateralization rate of 500% — meaning staking 5 SNX to get 1 sUSD, and forced liquidation occurs when the collateralization rate touches 200%. This contradicts the original intention of derivatives trading.

Finally, since all trading in decentralized projects is on-chain with clearly queryable data, this violates the needs of large institutional traders who wish to hide their positions and contract addresses.

In summary, although there are various issues with the current development of decentralized exchanges, with the continuous improvement of Layer 2 infrastructure, decentralized derivatives trading is about to reach its peak. However, this is insufficient to support decentralized derivatives trading surpassing centralized exchanges. In the future, the two will exhibit a complementary relationship like DEX and CEX, rather than being mutually destructive.

Disclaimer

This article may contain product-related content not applicable to your region. This article is intended to provide general information only and does not take responsibility for any factual errors or omissions herein. This article represents only the author's personal views and does not represent the views of OKX. This article is not intended to provide any advice, including but not limited to: (i) investment advice or investment recommendations; (ii) offers or solicitations to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. Holding digital assets (including stablecoins) involves high risk, may fluctuate significantly, and may even become worthless. You should carefully consider whether trading or holding digital assets is suitable for you based on your financial situation. For questions regarding your specific situation, please consult your legal/tax/investment professional. The information appearing in this article (including market data and statistics, if any) is for general reference only. While we have taken all reasonable precautions in preparing these data and charts, we assume no responsibility for any factual errors or omissions expressed herein. © 2025 OKX. This article may be reproduced or distributed in its entirety, or excerpts of 100 words or less from this article may be used, provided such use is non-commercial. Any reproduction or distribution of the entire article must also prominently state: "This article is copyrighted © 2025 OKX, used with permission." Permitted excerpts must cite the article name and include attribution, for example "Article Name, [Author Name (if applicable)], © 2025 OKX". Some content may be generated or assisted by artificial intelligence (AI) tools. Derivative works or other uses of this article are not permitted.

Show More

Recommended Reading

OKX Pay: Opening a New Era of Next-Generation Crypto Payments

The choice of tens of millions of users, register with OKX and enjoy the ultimate trading experience and diverse wealth management products. A letter from OKX CEO Star: Today, we are officially launching the first version of OKX Pay to over 100 million global users. As the industry's first payment application that truly achieves the integration of non-custodial and compliant features, OKX Pay will be embedded in the OKX App, currently available to select markets, and expected to fully launch within months

March 22, 2026

New Chapter: Building Next-Generation Financial Infrastructure Together

The partnership between OKX and Intercontinental Exchange (ICE) is an important moment for OKX and equally significant for the evolution of the entire digital assets market. ICE establishes and operates the world's most important financial infrastructure, including the New York Stock Exchange as well as global derivatives and clearing platforms. This investment by ICE in OKX and joining our board reflects both parties' shared belief — that digital assets technology will play a crucial role in financial markets

March 10, 2026

Tribute to Another Year of Forging Ahead

As OKX's CEO and also a builder who remains true to our original mission, I proudly look back on the remarkable growth and progress OKX has achieved this year. Despite numerous challenges, 2024 was a year filled with focus, innovation, and resilience. We not only expanded and optimized our products but also made significant progress in launching transparent and compliant localized businesses, while further strengthening our global management team. Notably, after experiencing

January 29, 2026

2025: Steady Progress Toward Financial Freedom Together

— Year-end letter from OKX Founder and CEO Star to global users "Financial freedom" is often misunderstood. It does not mean no rules, but rather having the right to choose even when rules exist — and when the system is truly tested, it remains reliable and effective. This is exactly what we have remained focused on throughout 2025. First, I would like to extend my sincere gratitude to our global clients, partners, and regulatory authorities

January 16, 2026

OKX Officially Launches in Germany and Poland

Author: Erald Ghoos, CEO of OKX Europe Today is significant for OKX — and for crypto users across Europe. We have officially launched fully compliant centralized cryptocurrency trading platforms in Germany and Poland! For us, this is not just a geographic expansion, but a commitment to building the cryptocurrency future the right way: securely, transparently, and meeting local needs. If you are in Germany

October 21, 2025

Partnership Upgrade! OKX Partners with Standard Chartered to Expand European Market

On October 15, OKX Europe CEO Erald Ghoos stated that OKX is expanding its strategic partnership with Standard Chartered to the European Economic Area (EEA). Earlier this year, OKX first partnered with Standard Chartered in the UAE to launch the collateral mirroring program — an initiative that

October 15, 2025